I

DON'T KNOW HOW MUCH CLEAR IT GETS THAN THIS:

By

Scott Lanman and Craig Torres

Jan. 7 (Bloomberg) -- U.S. regulators including the Federal

Reserve warned banks to guard against possible losses from an

end to low interest rates and reduce exposure or raise capital

if needed.

“In

the current environment of historically low short-term

interest rates, it is important for institutions to have robust

processes for measuring and, where necessary, mitigating their

exposure to potential increases in interest rates,” the Federal

Financial Institutions Examination Council, which includes the

Fed, Federal Deposit Insurance Corp. and other agencies, said in

a statement today.

Let me point out a few things.

- We have never seen a crash and rebound in US stock

market history like what we have just experienced, except once. That

"once" was 1929/1930. What followed next was a grueling

grind - not a crash, but a grind that never ended, and in which the market

lost more than 80% of it's value. Those who argue "the

bigger the dive the bigger the bounce" forget that the only true

comparison against what we have just seen was in fact the prelude to a

grinding 90%+ overall decline.

- If you believe in "long wave" cycles - that is,

Kondratieff cycles, we have precisely followed the

several-hundred-year long pattern though its latest incarnation, with the

1982-2000ish period being "Autumn." Winter follows fall. These

cycles seem to happen mostly because all (or essentially all) of the

people who lived through the last cycle's horrors are dead. Unless we have

found a way to break a cycle that has endured far longer than our nation,

we're right where we should be - which incidentally aligns with what

happened in 1929/30 as well. This means that while there may be ups and

downs we have not bottomed - not by a long shot - no

matter what people tell you.

- Interest rates can only go up from zero. That should be obvious.

Rising rates are not positive for equities and multiple expansion.

- The Financials are getting a tremendous bid the

last few days, presumably on the premise that "employment is at least

somewhat stabilizing." With zero short rates and a steep yield curve,

this means they make a lot of money. But rates cannot stay where

they are if in fact the economy is recovering, and if the long end rises

it will choke off housing.

- At the same time people are rotating into a sector The Fed

and regulators just said will be forced to constrain its profits

people are fleeing the stocks (tech) that have been on a

tear. This is exactly backward based on the news flow.

Are The Fed and Regulators lying or is the "optimism" incredibly

misplaced (and even stupid if they're rotating out of winners for what

were just announced would be losers!)

- P/Es are at record levels. Yes, that's on "as

reported" 12 month trailing, and it is down materially since one of

the two "disaster quarters" is now gone. But even with the other

gone (which it will be in another month) we will be trading at

somewhere around 40 or 50x earnings, an utterly unsupportable level and

above where we were in 1999 - just before the entire market fell apart.

Even on "operating earnings" we're trading at 24 times -

outrageously overvalued from a historical perspective.

We

also have the BIS calling in bankers to warn them that they've changed nothing

in their behavior (gee, really?) and China

making a serious attempt to pop their property bubble (must be nice to

actually pay attention to such things, eh?)

For today, "party on Garth" in

equities.

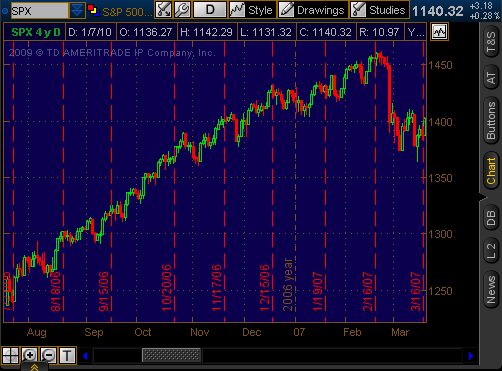

Let me simply remind people that what got

me writing The Market Ticker was this event - something that I missed

the signs of because I was overly complacent, just as people are being

right now.

That was 2006 and into 2007, remember?

Straight up - right up until it wasn't,

and 60 SPX points came off in one day. That warning (and mine when I started

writing) was ignored by a whole lot of people too who thought it was a

"blip."

Uh, no, it was a warning and those who

failed to heed it got their heads handed to them.

Don't worry folks, it can't happen again.

Remember, The Fed has our back, just as they did in 2006 when they told us

there was nothing to worry about in the summer when we got the swoon (remember

that? I do - and bought into it!)

The picture now is actually worse

than it was in early 2007. In early 2007 we had solid employment, we still had

a reasonable housing market although it had slowed some, GDP was positive and

we had just come off a GREAT Christmas season with

extraordinary profits and sales. In addition we were running ~350 billion in

deficits, not $1.6 trillion (estimated for FY10) nor did we have to roll and

issue over $2 trillion of treasury debt (to someone!) in the next 12 months.

Now we have the regulators issuing formal

warnings about bank liquidity and interest rate risk (no

really, you think that might be an issue with that sort of issue behavior?)

while at the same time formal liquidity support in the form of monetization

along with stimulus spending is slipping away - the source of the liquidity

that fueled the rally from March.

Ignore all this if you're brave - or

stupid.

PIMCO

isn't. Bill Gross sees the same thing I see.