The markets were

down a bit yesterday and, according to Bloomberg,

they were down due to fears of the stress test results. I don't fear them; I

fear what they hide. I fear that a reported 10 out of 19 banks failed when the

tests were not at all stringent enough. I fear that the government will

soft-pedal the results to make them bad enough to have a tad of credibility but

not so bad that people run for the exits. Don't buy my word for it, others are

saying the same, including Nouriel Roubini.

Nouriel has been complaining for weeks on how the worst case scenario in the

stress tests is already rosier than reality. Go figure?

I noted yesterday

that I do not see a recovery of our economy any time soon as 70% of our GDP is

consumer spending and that is going to suck wind for years to come. One point I

made was that wages were stagnating at best and likely decreasing - not to

mention unemployment, capital destruction and the like. Michael Shedlock

provides us with a good bit of detail on this point. As he points out, wages

are contracting in the U.S., U.K. and Japan - three major

economies. This cannot be good for these countries' economies or the multiple

countries that supply them products.

I do recommend that

you go to the linked site as there are a couple of other significant points

covered there, with nice charts. For example, Mish

notes it is presently taking a significant percentage of disposable income

(19%) to service household financial obligations, meaning less is left over for

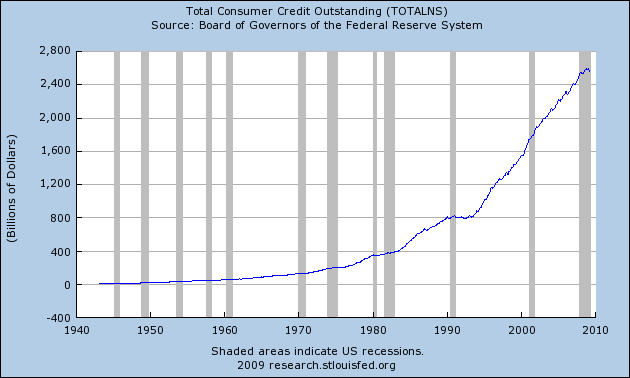

consumer spending - especially with people starting to save. Here is one very

telling chart from the post showing that we are drowning in more debt now than

ever before. Gee, I see a recovery around the corner. Yep, there it is.

In case you are

wondering whether the individual strain on spending in the U.S. is having any

significant impact on GDP growth, the answer is a definite yes! Nominal GDP growth has turned negative YOY

for the first time in 50 years. And the markets have gone up significantly

since the March 9 bottom. Go figure?

So what do we do to

deal with the most significant debt crisis ever to face our country? You got

it, we incur more debt. Now this debt is on the government level and it is

getting seriously over the top.

Now if the

government were taking on this debt to give the money to taxpayers so they can

pay off debt and deleverage, that would be one

thing. But precious little is going to individuals to deleverage.

Rather it is going to the bastards that got us here so that they can promote

more lending and individual debt. Think about that long and hard. I have and I

simply cannot convince myself of the sense of it. If instead we gave money to

individuals so they could deleverage then they

would not need to spend their own increasingly sparse dollars to deleverage.

This is not perfect, but at least new debt on the government level is removing

debt from individual balance sheets. At least those paying for it (taxpayers)

get the benefit.

I have said here

often that Americans hunkering down is a good thing. I just said yesterday that

Americans saving is tough on the economy in the short term but good in the long

term. I stand by these comments, but let me add a caveat. If we all start

selling what we have to make money and start saving too much all at once and

all start spending significantly less, it does run the risk of creating a

dangerous spiral. Deflation starts in as prices drop to try to lure an ever

more frugal consumer. Yet deflation makes the

debt more onerous. The cycle is one that is difficult to break when it starts.

Thus the occasional statements by the Administration that

Americans should not stop spending and its desire to get credit flowing again.

They should explain this a bit better and realize Americans need to deleverage, not build debt, though we probably need to

do it slowly to avoid potentially dangerous spirals. The attached link, while a

bit long, explains this in much better detail. This is something important to

understand, so I recommend the full read of the linked article. It goes through a number of other

interesting points but it ends with a discussion of the possible spiral. We are

my friends in very delicate times. Damned if you do, damned if you don't. Yet

the markets are up significantly since March 9. Go figure?

Still, given the

danger of a spiral forming if Americans seek to save too much and deleverage too much during a time of reduced jobs and

wages, you would think the Administration would be doing everything it could to

help the average "Joe the plumber" to deleverage

(and pay his taxes), so that Joe could perhaps spend a bit more of his income -

as small as it might be. If the government incurs debt for individuals to

reduce debt, that is not perfect but it is better than the government

incurring massive debt to support more lending. Moreover it is significantly

much better than taxpayer dollars going to big bank dividends, executive

bonuses and the like. Even if all the government

largess to banks led to more credit availability, we do not need lending, we

need the reverse. I am truly praying that common sense sets in for the

Administration soon.

Real Estate - At a Bottom?

On occasion

I have noted I see no true bottom until housing bottoms. With job losses,

significant individual debt to deleverage and a

variety of other ills, a housing bottom is just the beginning of what we need.

Nonetheless, it does not look like we are there just yet even on housing. My

favorite site on housing, and some other issues, Calculated Risk, notes some recent reports confirming same.

Part of the problem

is that just when we feel like we have reached a housing bottom, which I

anticipate toward the end of this year, we will enter into the peak years for

option ARM resets (adjustable rate mortgages that let the lenders pay less than

interest), which will lead to more foreclosures and more downward pressure.

This is a major issue for Wells Fargo (WFC) and the likely

reason it will be one of the 10 banks needing more capital.

And last but not

least, I leave you with a very much worth while link to Zero Hedge. They go through in very nice detail some of my

concerns. I agree with them on pretty much all their points. It is a long post

by them but well worth the read. Well balanced, informative

and educational - just what I like.

And so I feel I am

repeating myself. At least as you can see from the linked materials above I am

not alone in my thoughts. Still, I think people are tired of the negative news

and would prefer to hear media lies to make them feel better. At least that is

one comical take on the matter.

Disclosures: None.