The

Fed's Shell Game Continues...

Chris

Martenson

Executive

Summary

- Record-breaking Treasury auctions continue to go

off without a hitch, thanks to massive foreign participation.

- However, the amounts reported to be bought in

the auction results do not match the Custody Account or TIC report

amounts.

- The Fed is allegedly all done buying MBS and Treasury

paper. This cuts off an important source of liquidity for the Treasury,

commodity, and stock markets.

- How will these markets respond to a liquidity

drought?

April is upon us. I need to take a

moment to re-analyze the data to see what might happen now that the stimulus

money has worn off, and, more importantly, now that the Federal Reserve's

massive Mortgage Backed Security [MBS] purchase program is over.

This is important for a variety of

reasons. The first is that the enormous flood of liquidity that the Federal

Reserve injected into the financial system has found its way into the Treasury

market, supporting government borrowing and also lowering interest rates for

the housing market. How will the Treasury market respond once the liquidity

spigot is turned off?

The second is that this flood of

liquidity has supported all sorts of other asset markets along the way,

including the stock and commodity markets. What will happen to these when the

flood stops? Will the base economy have recovered enough that the financial

markets can operate on their own? Will stocks falter after an amazing run? Or

will the whole thing shudder to a halt for a double-dip recession?

Back in August of 2009, I wrote

that the Federal Reserve was basically just directly monetizing U.S. government

debt by buying recent Treasury issuances as well as Mortgage Backed Securities

[MBS].

Here's the conclusion from that report:

The Federal Reserve has effectively

been monetizing far more US government debt than has openly been revealed, by

cleverly enabling foreign central banks to swap their agency debt for Treasury

debt. This is not a sign of strength and reveals a pattern of trading temporary

relief for future difficulties.

This is very nearly the same path that

Zimbabwe took, resulting in the complete abandonment of the Zimbabwe dollar as

a unit of currency. The difference is in the complexity of the game being

played, not the substance of the actions themselves.

When the full scope of this program is

more widely recognized, ever more pressure will fall upon the dollar, as more

and more private investors shun the dollar and all dollar-denominated

instruments as stores of value and wealth. This will further burden the efforts

of the various central banks around the world, as they endeavor to meet the

vast borrowing desires of the US government.

My surprise at all of this has been

twofold. The shell game has continued this long without the bond market calling

the bluff, and I am baffled by the extent to which the other world central

banks have both enabled and participated in this game

Part of the explanation behind this

unwavering support for the dollar and U.S. deficit spending by other central

banks lies in the fact that other Western and Eastern governments are equally

insolvent. It's possible that they feel they really have no choice but to play

along, because the alternative would be to inflict a vicious and deeply

unpopular austerity program on their own country, while everybody else is

partying on thin-air money. Who's going to be the first to do that? Nobody,

that's who.

The Size of the Problem (or is it Predicament?)

Let's begin by noting the massive

growth in the Treasury auctions over the past few years. Where once we required

a few hundred billion per year of new, incremental borrowing to fund the fiscal

gaps, we are now borrowing more than a trillion each year. Where the total size

of all auctions (including rollovers) was a couple of trillion each year, it is

now approaching ten trillion.

The way I prefer to track this is at

the source. The media does an especially poor job of communicating accurate

government deficit figures. They simply relate the cash deficit, which is how the

government reports it. However, the true borrowing needs due to the deficit are

best, and most easily, tracked by simply noting the increase in the "debt

held by the public" portion of the federal debt. Why the press misses out

on this year after year is beyond me.

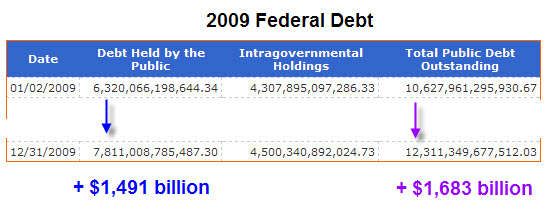

We know that in 2009, the incremental

borrowing needs of the federal government (give or take a few billion, due to

timing) must have been equal to the reported growth in the "debt held

by the public" portion of the federal debt.

That figure for 2009 was $1,491 billion

(or $1.49 trillion):

Recall that the total federal debt

consists of the two components in the table above; 'debt held by the

public' and'intragovernmental holdings.' The former represents

the size of all outstanding Treasury debt, and the latter represents money that

the government has borrowed from itself but owes to various retirees and

entitlement beneficiaries.

When the value of 'intragovernmental

holdings' rises, it means that cash was borrowed from the entitlement

programs and used to fund government operations. If it rises, as we see above

in 2009, then more money is coming in than going out. If it is stagnant, then

money coming into the programs is being equaled by money leaving. If, heaven

forbid, it falls, that means that the programs are now cash-flow negative to

government coffers and more money is being paid out than is being taken in,

which is our current situation here in 2010 (see next table below).

At any rate, for our purposes, we need

to try and figure out where a record-shattering $1.49 trillion in fresh

Treasury issuances went in 2009. Who bought them? How much went to foreign

buyers, and can we expect them to buy more?

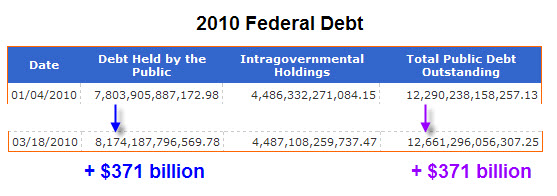

And so far in 2010, we see that we are

on track for another ~$1.5 trillion round of fresh borrowing:

Taken together, this means that in only

two short years, 2009 and 2010, as much new Treasury debt will be auctioned off

to the public as was outstanding in 1995. Since government borrowing never gets

paid down, at least in modern history, it means that the last two years have

seen as much borrowing as happened over the period in which electricity was

strung to every house, the highways were built, and our population tripled.

What can we point to that was created over the last two years to rival those

accomplishments?

Even more interestingly, we note

something quite extraordinary in that table above: Through the middle of March,

the intragovernmental holdings have not increased, which indicates

that expenditures are equal to revenues for the entitlement programs. This has

not happened for decades. It means that from a cash-flow standpoint, the U.S.

government has lost an important source of liquid operating cash. This is an

enormous inflection point in the data series. Instead of providing cash to

government operations, the entitlement programs are now on the verge of

draining cash. The importance of this shift cannot be overstated.

Which brings us to the most important

question of them all, which concerns the continued ability of the U.S. and

various other world governments to fund their deficits. It is my contention

that too few people are thinking about the possibility that the U.S. government

could face a funding crisis at some point, which means that it's a clear and

present danger.

U.S. Treasury Auction Results

Let's look at the Treasury auction data

since 2009 to see what it can tell us. To begin with, an auction may do a

couple of things. It may sell brand-new debt to raise new cash, it may

"roll over" past debt that is maturing, or both. So where 2009 saw

$1.49 trillion in new debt sold, the total volume of the Treasury

auctions was far larger, when we add up all the roll-over activity.

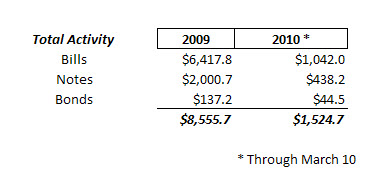

Here's the data for the total activity

2009 and some of 2010:

(Note: This data excludes TIPS and

cash management bills, so these numbers are actually smaller than the complete

total.)

The table above tells us that while

$1.49 trillion in new debt was issued in 2009, more than $8.5 trillion in total

activity took place. That's how much cash had to flow through the Treasury

auction market for it to function.

This illustrates why a failed Treasury

auction will be avoided at all costs. Any interruption to the trillions and

trillions of dollars flowing through the Treasury market each year would cause

an immediate and enormous train wreck that would ripple through the entire

world's financial system (and trigger an avalanche comprised of hundreds of

trillions of dollars of interest-rate derivatives). A failed auction is simply

not an option for the Fed or the Treasury Dept.

In 2010, more than $1.5 trillion in

total activity had already occurred by March 10th. Once we mentally

add in this year's likely borrowing, we might expect a grand total of some $10

trillion in total activity to take place by the end of the year. In 2003, the

total activity of this market was only some $3.4 trillion. If you plot out the

growth in activity, it looks like an exponential chart.

With government deficits in the

trillions stretching as far as the eye can see, and with an ever-increasing

reliance on short-term debt, this trend is set to increase going forward.

Where It All Went

So now we know that nearly $1.5

trillion of new Treasury debt went out the door in 2009, along with another

$371 billion in 2010. But where did it all go? Who bought it? Can we count on

them to keep buying?

Here the data is not as clean and clear

as I would like. There is quite a bit that is difficult to determine, based on

the way that that data is collected and reported. While it may not be the

intent of the data gatherers to hide anything, that is the result.

In terms of the disposition of the

$1,491 billion in Treasury bonds bought in 2009, here's what we do know:

- The Fed bought $300 billion of them, all

long-dated securities.

- According to the TIC report, foreigners bought

$617.6 billion.

- The rest, 'the plug factor,' was assigned to

"households" by the Federal Reserve, accounting for more than

$530 billion.

There are many who have questioned

whether "households" were in any position to park more than 100% of

their entire personal savings into Treasury instruments, but even the Fed tells

us that this is a plug category, meaning anything not identified as going to

itself or foreigners is assigned to this category. The Fed has no idea how many

Treasuries "households" bought in 2009; it only knows how many are

not otherwise officially accounted for and that it should assign the difference

to "households."

The truth is, we have no idea where

that half-trillion in Treasuries went. My best guess would be that they mainly

went to large banks (probably even the primary dealers themselves) to a large

degree, especially those that sold MBS to the Fed. In keeping with the

"shell game" concept, the only entities out there with a

half-trillion lying around in 2009 probably got it from the Fed.

An asterisk in this story of where

those Treasuries went concerns the difference between what the Treasury reports

that foreigners bought (in the TIC report) and what the Fed says foreigners

accumulated in the Custody Account. Unfortunately, these two reports overlap to

a large degree, but not completely. This is a critical bit of investigation to

perform, because it is so important that foreigners continue to buy U.S.

Treasury debt. In 2009, the Custody Account holdings of Treasuries increased by

$572 billion, while the TIC report said foreigners bought $617.6 billion, and

we are unable to account for the whopping $45 billion difference between the

two numbers.

The Custody Account

I described the Custody Account in some

detail back in August of 2009 in The Shell Game, so

I won't rehash how it operates here, except to say that it is basically a

gigantic brokerage account held by the Fed on behalf of foreign central banks.

In order to understand foreign buying

habits when it comes to Treasuries, we need to peer into both the TIC and the

Custody Account. When we did this last August, here is what we found for the

Custody Account:

The story in August of 2009 was one of

rapid, uninterrupted growth in the Custody Account, seemingly without any

concern or regard for the financial crisis happening then.

Today we find that during 2010, the

Custody Account has not grown very robustly:

I am immediately drawn to the fact that

the foreign Custody Account has been, well, a little flat lately (as marked at

the end by the blue line at the top right). However, it's also been a little

flat at other times, which I have marked with dark horizontal lines, so perhaps

this is a relatively normal occurrence. Overall, perhaps we should be most

impressed with the >250% growth over the past seven years(!).

Think of this $3 trillion debt as the

portion of U.S. government debt that is owed to a foreign credit-card firm.

Someday that's going to have to be paid back, and, no, it doesn't bode well for

the future prosperity of the U.S.

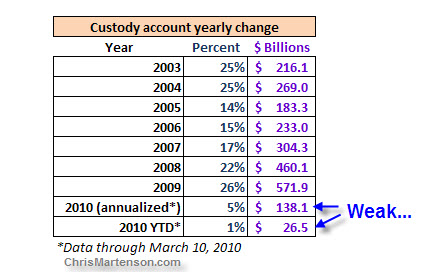

Here's the Custody Account in table

form, which reveals that 2010 is shaping up to be the weakest year in a long

time:

I'm sorry, but a 5% growth in the

Custody Account just isn't going to cut it for a country with a

multi-trillion-dollar borrowing habit. So far, the Custody Account has only

increased by a paltry $26.5 billion in 2010. That's a real cause for concern,

and it makes me wonder about the recent upward volatility in Treasury yields.

Now, the Custody Account consists of

both Treasuries and Agency debt. Teasing this apart into its components, we

find that total Treasury accumulation into the Custody Account has been a quite

anemic $24.6 billion in 2010, which is more or less the same amount that was

accumulated during a single week back in 2008 and 2009.

Let's compare this $24.6 billion to the

$371 billion of new Treasury debt sold in 2010 - it's only 7% of the total. But

we are told, week after week, that foreigners (via the "indirect

bid") have bought on the order of 40% of each auction, or nearly $150

billion. What gives?

Like here in this recent auction, where

39% of a single auction totaling $16.6 billion went to the indirect bidders:

![]()

What we are seeing here is a very large

(and growing) disconnect, between the proportion of Treasuries that are said to

be bought by foreigners in the Treasury auction result announcements, and

what's showing up in their official TIC and Custody Accounts.

I am increasingly concerned that this

gap reflects a growing accumulation of Treasury issues by entities funded for

this purpose by the Fed's magic thin-air checkbook. If so, then the danger

would be the response of the market and the reaction of various countries when

that becomes common knowledge.

For now, it is clear that 40% of US

Treasury auctions are not being bought by foreigners, at least if the TIC and

Custody Account reports are to be believed.

Perhaps the growth in the Custody

Account will resume and my concerns will amount to nothing, but the first

quarter of 2010 is shaping up to be somewhat of a gigantic disappointment in that

department. Unfortunately, the TIC report is lagged by a couple of months, so

we won't have the March numbers for comparison until the middle of June. My

guess is that the TIC report will also show weakness in the foreign

accumulation of Treasury debt, but we'll also be taking a look then, just to be

sure.

The concern here is that the Custody

Account is reflecting early signs of waning foreign interest in U.S. debt. If

(or when) we finally reach the point of saturation in this story, everything

will change rather dramatically.

From Zero Hedge, we have this nice summary

of the debt auctions coming up for next week:

The Treasury just announced the auction

schedule for next week: a total of $165 Billion in gross issuance of which $74

Billion in coupons, and $8 billion in a 10 Year TIPS reopening.

·

$28

billion in 3 Month Bills, Auction date April 5

·

$29

billion in 6 Month Bills, Auction date April 5

·

$26

billion in 52 Week Bills, Auction date April 6

·

$40

billion in 3 Year Bonds, Auction date April 6

·

$21

billion in 9 Year 10 Month (reopening), Auction date April 7

·

$13

billion in 29 Year 10 Month (reopening), Auction date April 8

·

$8 billion

in 9 Year 9 Month TIPS (Reopening), Auction date April 5

The fact of the matter is, the US

government is now conducting weekly Treasury auctions that are as large as

quarterly auctions were just a few years ago. Exponential increase, anyone?

$165 billion in a single week is an enormous pile to unload.

What I Am Always Looking Out For

Long-time readers know that I am

constantly on the lookout for a specific pair of market signals above all

others, because its arrival will signal that a new game has begun. That pair

comprises a simultaneously falling US dollar index and rising Treasury interest

rates (signaling falling Treasury bond prices).

In essence, this pair will signal to me

that some major player, perhaps China, has decided to sell its Treasuries and

take its money home, thereby driving down the dollar. This is critical to me,

because it will mean that the US will have begun its long date with funding

difficulties. Either interest rates will have to rise dramatically to attract

new lenders (thereby killing the nascent recovery of the housing market and our

entire credit-fueled economy), or the Fed will have to begin monetizing at an

even faster rate than before.

In short, we'll be facing a period of

profound austerity, raging inflation brought about by currency devaluation, or

both. In truth, I cannot imagine any possible way for the U.S. to pay off its

current official debts in current dollars, so I feel this outcome is merely a

matter of time. However, it could be a long time, and we must also be prepared

for that.

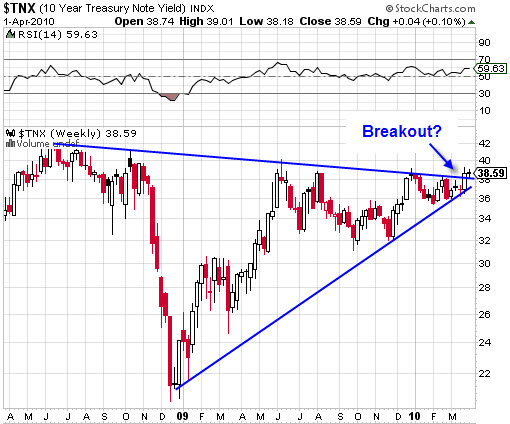

In the past week, there was a bit of

excitement over in the Treasury market because there were two days of hard

selling in a row. This led to Treasury yields spiking and possibly breaking out

over a two-year trend line:

The Treasury market immediately settled

down right after these two days of selling, but something significant had

clearly happened. During this period, the dollar also rose quite handily, so my

"signal pair" was not in play and I did not issue an alert, nor did I

become overly concerned. However, I did sit up and take notice and am

following bond market signals with just a bit more focus these days.

A rapid rise in long-term interest

rates here would be just about the last thing the Fed would want, as that would

put pressure on stocks and commodities, and harm the housing recovery, such as

it is. So I doubt that the rate rise was planned or welcomed.

I am keeping a very close eye on the

Treasury market right now and will alert you if anything breaks suddenly or

crosses the threshold to actionable news.

One Possible Scenario

Although I am not convinced that I have

access to good data, it would seem that China is in a serious bubble. Or,

rather, a series of bubbles, including real estate in several metropolitan

locations and manufacturing overcapacity. Several recent commentators have been

adding up the facts as we know them, and it seems plausible to suspect that

China is deep into bubble territory.

China also happens to hold $890 billion

of US Treasuries (as of January 2010), as well as some amount of MBS stashed in

the Fed's Custody Account (I don't have access to the necessary detail to say

how much), so we'd be close if we estimated that China held $1 trillion of

official US debt.

One scenario that I think has a chance

of upsetting things would be for China to experience a bubble-bursting crisis,

the mitigation of which would necessitate a need for liquid cash. By this, I

mean an event (or set of events) that would essentially force China to begin

unloading their Treasury holdings.

Under this scenario, we'd see immediate

selling pressure in the Treasury market, leading to lower prices and higher

yields. I think this event would be sufficient to rip the cover off the

Treasury market and expose the extent to which the market has been supported by

central banks more than legitimate market players and expectations.

So another thing I am keeping an eye

out for is any sign that China is experiencing a bubble-bursting event. Here I

track the Chinese stock market, the Baltic Dry Index (as a crude measure of

export activity), and the news.

Conclusion

With a stagnant Custody Account reading

and underwhelming TIC reports, it seems unlikely that that foreigners are going

to be able to digest the volume of Treasury auctions that are coming up this

year. We've already seen a nice breakout on yields. With everything I know

about Fed policy at this point, I can assure you that a sudden jump in rates on

the long end was not in the Fed's plans for last week.

My concern is that the mysterious

indirect and direct buyers that have been showing up at Treasury auctions

lately may be none other than the Fed itself or its proxies, hidden by some

slight shell game or another.

There simply seems to be no other

explanation, given the perilous state of the global economy. Where is all this

capital coming from, if not central banks? From earnings? From exports? From

legitimate economic savings? From private individuals (during a major stock

bull run)? None of these explanations matches the volume of borrowing that we

are seeing in the U.S. Treasury market, let alone worldwide.

The simplest explanation is that

central banks are somehow providing the necessary liquidity to support the

various governmental bond auctions that are happening around the world. The

U.S. story does not add up and provides enough of a smoking gun to suggest that

there are (at the very least) non-transparent buyers for the massive,

record-breaking Treasury issuances we've been seeing lately.

If, or when, these deceptions are

revealed, I predict that we will experience a pretty significant market

dislocation that will take the form of a chaotic bond market, with yields that

rapidly gyrate higher, currency perturbations that will shake markets, and an

extended banking holiday, with capital controls imposed until a nightmarish

derivative mess is unsorted.

Of course, these are just my hunches at

this point. Something is very much 'not right' in this story, but over the

years I have learned that strange market conditions can last longer than you

think possible and that things always seem to unfold more slowly than you might

initially suspect.

So I am prepared for two possible

scenarios: 1) a sudden change in the markets, and the alternative, 2) no change

at all for ten years or more. The first requires active financial and physical

planning, while the second requires developing the right sort of mental

patience. It is a tricky psychological balancing act, to be ready for anything

and nothing at the same time. I imagine that being on patrol in Baghdad during

hostilities was sort of like this, where nothing happened for 99% of the time,

but then IEDs made the other 1% of the time very, very interesting.

What will happen next? Nobody knows. My

advice remains the same as always: Stay tuned to the world's markets and

happenings for clues about what's unfolding, but make the necessary

preparations to increase your resilience to whatever might happen next.

The current market environment , where

everyone is seemingly convinced that a recovery is now all but assured, is both

encouraging and concerning. Encouraging because that's most likely true.

Concerning because sharp breaks almost always happen during periods of

complacency, when everybody seems to be looking the other way. In short, when

everyone is complacent, I get concerned, and when people get concerned, I try

to remain calm.

For now, there's a level of complacency

about Treasury auctions that I find very disturbing. There's really no way to

make the story add up properly - I mean, how could it, with $1.5 trillion in

new borrowing for two years in a row during economic weakness? - yet almost

nobody seems to be concerned about the implications of that line of thinking.

That is exactly the territory where

great fortunes are made and lost. At the very least, my wish is for you to

preserve what you have and to be able to maintain an even keel and positive

outlook, no matter what the future brings.

For myself, this means putting in 25

fruit and nut trees on my property (accomplished this past weekend), followed

by expanding the garden and installing solar and energy efficiency

improvements. We shall see if these turn out to be good uses for my capital and

time. For now, they provide me with the psychological sense of forward movement

and improvement, both of which are very important to me right now and worth

every penny to me all on their own.

Your faithful information scout,

Chris Martenson

Author's Disclosure: no positions